Happy New Year Café Hound! In 2015 we are going to try to add some new content on the site for the first time in a while.

One element of the new content is going to explore various data sources and statistical techniques regarding aspects of the coffee industry. A quick and dirty preview to this exploration follows below.

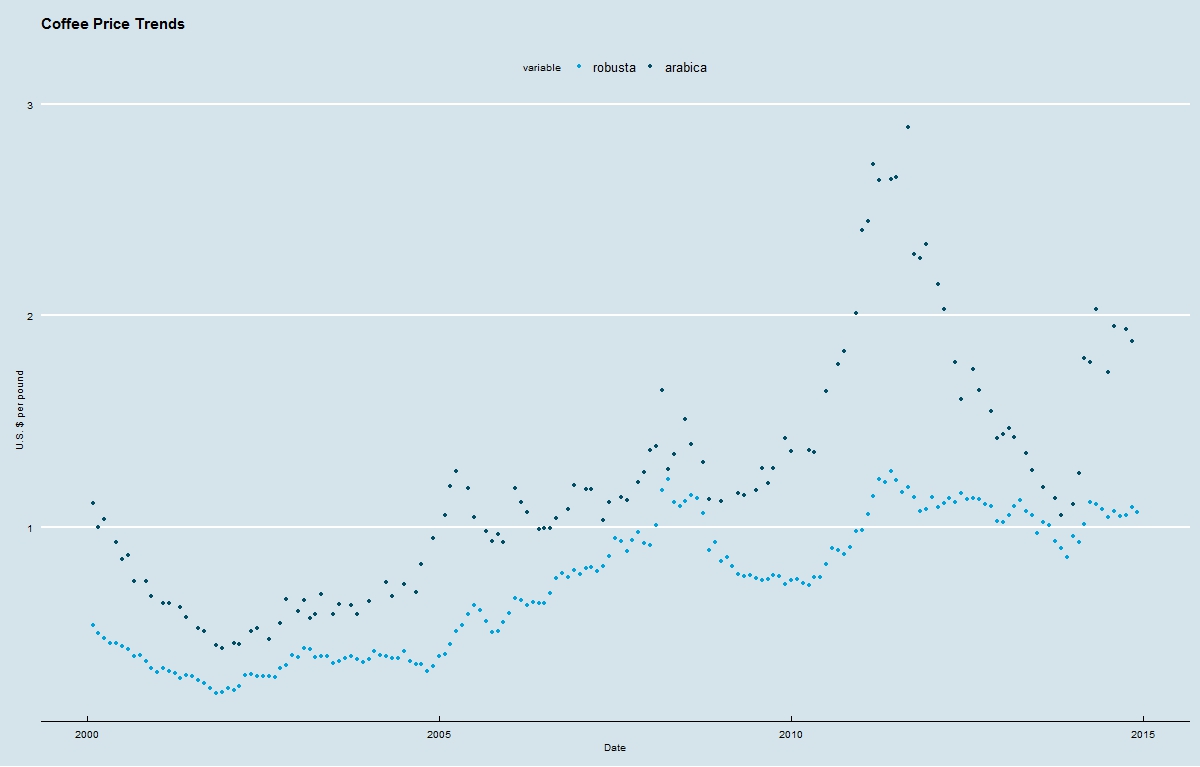

Cafe Hound developed a way to download daily price data for Arabica and Robusta coffee taken from daily settling prices (in New York and London respectively) for futures contracts. The unit of measurement is U.S. dollars per pound. We use a website called Quandl.com for the data. We use R as our data analysis software.

Prices for Arabica and Robusta Coffee

The overall trend line shows coffee becoming more expensive over the last fifteen years on average, although with a significant drop in price occurring after prices peaked in late August 2011.

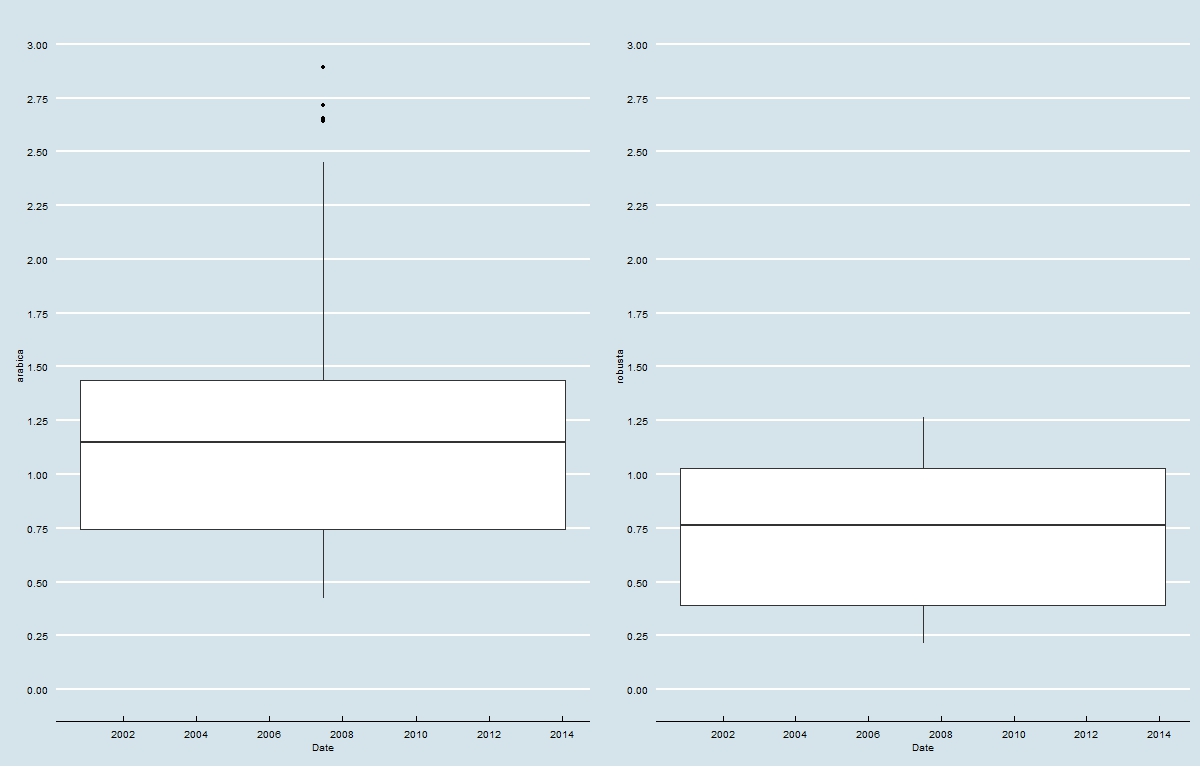

Price Range: Arabica vs. Robusta

Arabica coffee (starting in 2000) is three times more volatile than Robusta coffee in terms of price variance.

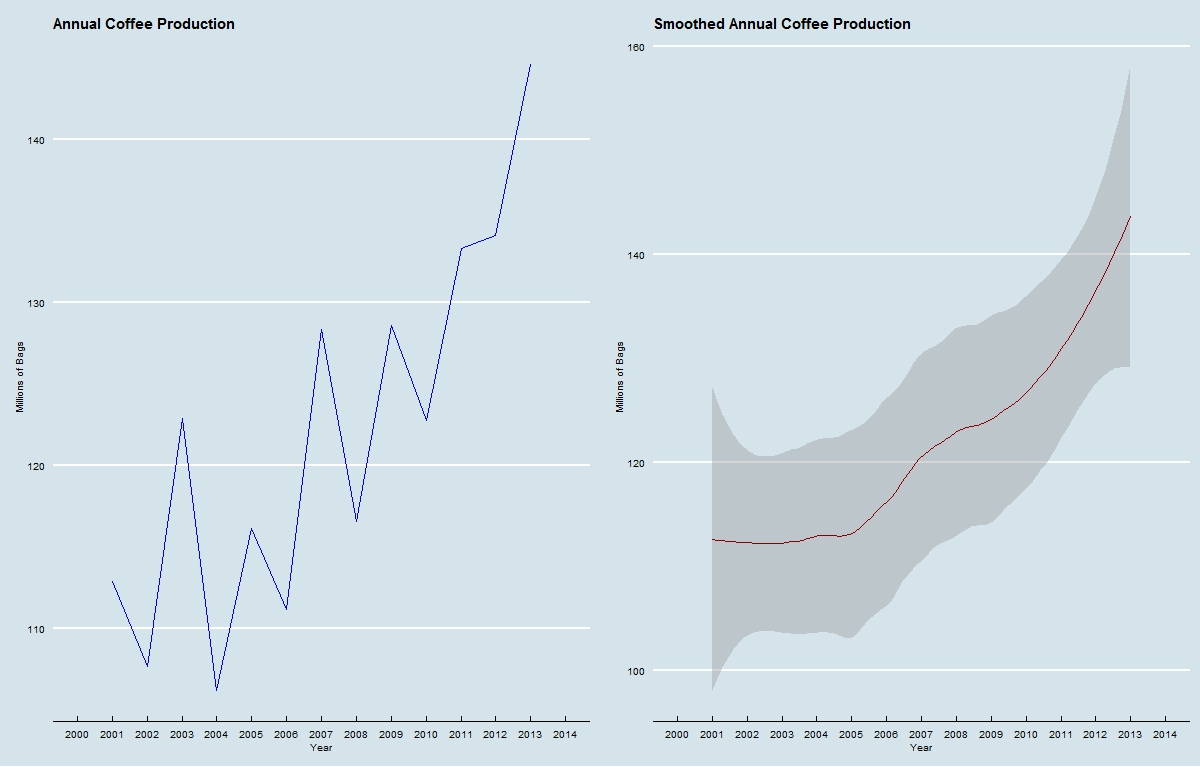

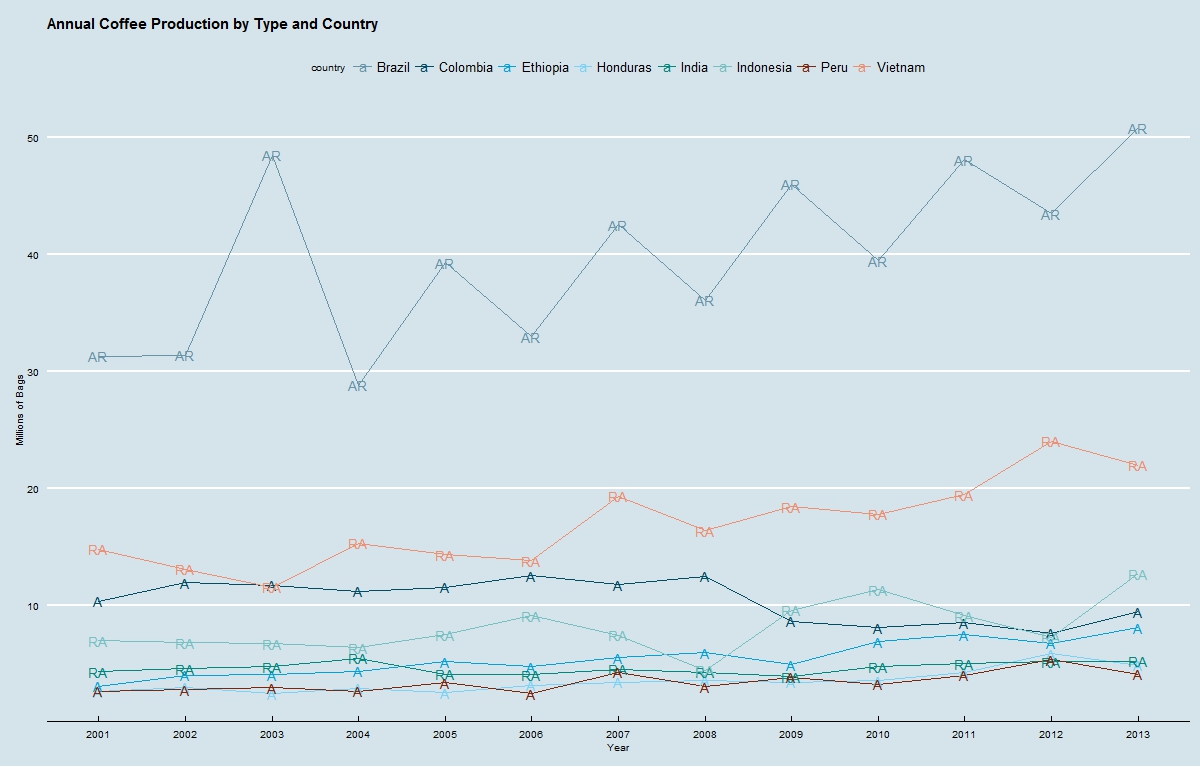

Now we will look at combined annual production of Arabica and Robusta coffee. This data was compiled with International Coffee Organization data that was manually inputted into a .csv file http://www.ico.org/new_historical.asp

Coffee Total Production by Year

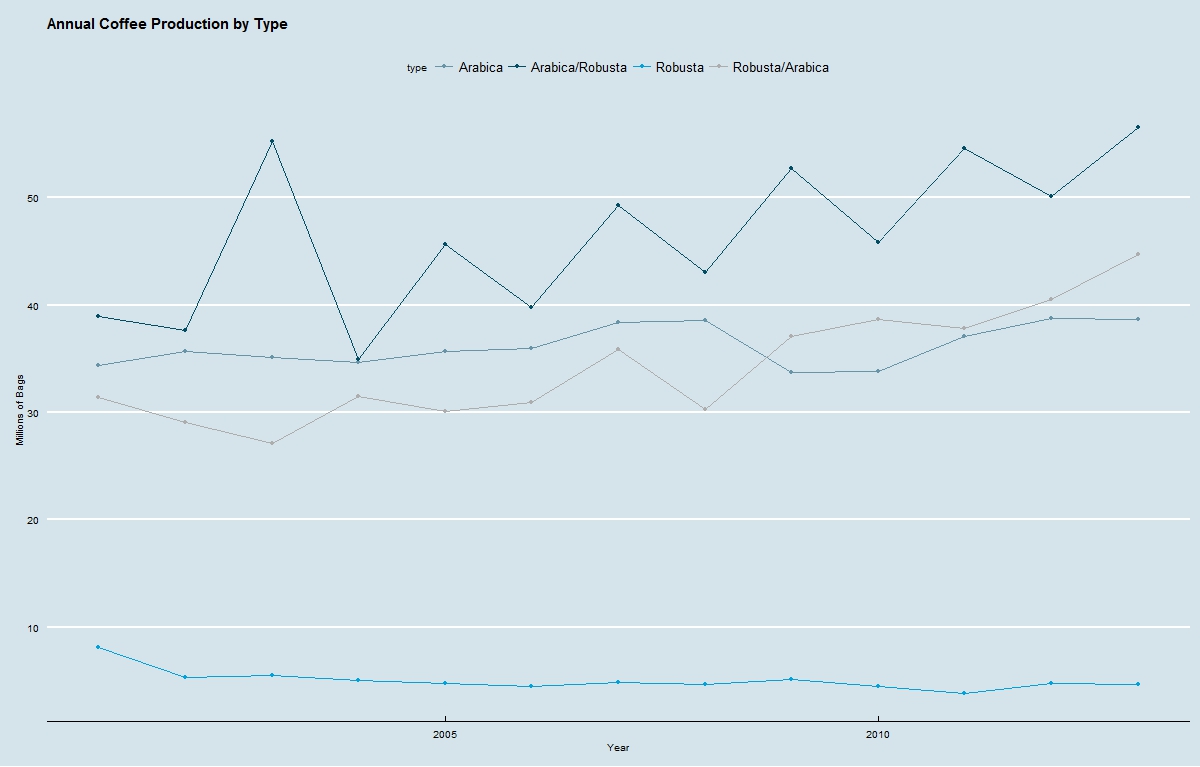

Coffee Production by Type

International Coffee Organization data isn’t as precise as it could be but it allows us to understand that the increased global coffee production is being produced in countries that are capable of growing millions of bags Arabica AND Robusta coffee in any given year.

Coffee Production by Type and Country

Increases in total production over the last few years appear to be driven by an increase in production from countries that are classified as producers of Arabica/Robusta and Robusta/Arabica coffee. In short, this means that countries that are producing both Arabica and Robusta coffee are responsible for driving the growth in global coffee supply. Specifically Brazil, Indonesia, and Vietnam appear to be increasing their share of global coffee production—likely focusing said production on the lower quality Robusta coffee.

That’s enough of a preview for now, but the basic takeaway from this information leads us to the conclusion that we should pay particular attention to the variables affecting production from Brazil, Vietnam and Indonesia if we want to forecast annual coffee production. However, at this point we haven’t explored the factors driving price enough to fully understand what we should be observing. More questions than answers at this point –meaning MORE analysis and exploration to come! Enjoy the New Year and keep checking in for more here at cafehound.com

Perhaps after completing decent market research, Starbucks realized that many in the growing global middle class aspire to an affluent lifestyle characterized by iPhone ownership, Starbucks specialty drinks, Coach products, and other premium brands. One of the most attainable products accessible to any income bracket is a simple cup of coffee and a snack. Juan Valdez, with its elegantly designed retails stores, has long taken advantage of growing wealth and a cultural disposition towards public life –of which the coffee shop culture plays a role. Since 2002, Juan Valdez retail locations have represented a place where folks can meet for business, for spending time with old friends and family, or on a date. It is seen as hip for younger generations while also as respectable and safe by older generations. It is also a source of national pride.

Perhaps after completing decent market research, Starbucks realized that many in the growing global middle class aspire to an affluent lifestyle characterized by iPhone ownership, Starbucks specialty drinks, Coach products, and other premium brands. One of the most attainable products accessible to any income bracket is a simple cup of coffee and a snack. Juan Valdez, with its elegantly designed retails stores, has long taken advantage of growing wealth and a cultural disposition towards public life –of which the coffee shop culture plays a role. Since 2002, Juan Valdez retail locations have represented a place where folks can meet for business, for spending time with old friends and family, or on a date. It is seen as hip for younger generations while also as respectable and safe by older generations. It is also a source of national pride.